The demise of Dick Smith has been all over the news. A recently issued report by McGrathNicol, the administrators of the Dick Smith group, has raised significant interest in respect of how Dick Smith was accounting for rebates, which has been reported on by Fairfax and The Motley Fool.

Both articles pose the question about transparency of financial reports, particularly in respect of retailers. It’s a good question but I think it misses the mark in respect of Dick Smith. I think most people want to know:

- How does an established and profitable business with revenues in excess of $1.3 billion go bust in the space of six months?

- Could the seeds of its demise have been gleaned from its recent financial information?

So, let’s take a look at that financial information and see what we can work out. In that process, let’s also find the applicable lessons for owners of small and medium businesses.

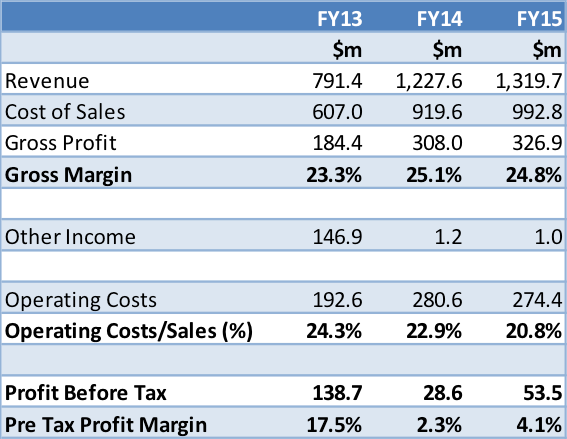

Dick Smith was an established, profitable and growing business …

Dick Smith stated operations in 1968. It was an established business. It was listed on the Australian Securities Exchange in November 2013. Its reported earnings are set out below, and as you can see:

- It was a growing and profitable business.

- Its gross margin was relatively stable at around 25%.

- Its operating costs as a percentage of sales were reducing.

- Its pre-tax Profit margin was increasing (FY13 was affected by one-off ‘other income’, so not representative of the underlying business performance).

So far, it’s a pretty good picture, albeit as the articles on the rebates make clear, perhaps a little too good to be true.

That needed cash to fund its growth …

Let’s take a look at a funds flow statement for Dick Smith. A funds flow statement compares the balance sheets of a business at two different points in time in order to establish where cash is coming from and going to.

It’s a great way for business owners to discover the true financial health of their business.

In this case, I am going to show you the funds flow for the two-year period from July 2013 to June 2015. By doing this, we will see a different picture emerging in terms of the cash use by the business. You can see the following:

- Cash contributed to / left in the business by owners of $12.6m.

- But, the increase in working capital to support the growth of the business used $92m of cash.

- And, the change in Non-Current Assets and Liabilities to support the increased number of stores used $23.1m of cash.

- This net funding requirement of $102.5m was met from using $16.9m of existing cash reserves and increasing borrowings by $85.6m.

This is a very different story to that presented in the profit and loss statement. But, I am not sure it is enough to explain the rapid change in fortunes that was to come.

But which it did not manage well …

A really good way to get a handle on how well your growth is being managed is to measure the change in your cash conversion cycle.

The cash conversion cycle is the time it takes to sell your inventory, collect your debtors and pay your creditors. It is a great measure to track, because it shows how your working capital is changing relative to the growth of your business.

The table below shows Dick Smith’s cash conversion cycle, with a comparison to its competitor JB Hi-Fi for the 2015 financial year. For Dick Smith you can see:

- Debtor days – the time taken to collect debtors – slowing from 4 days (FY13) to 15 days by FY15

- Stock days – the time taken to sell stock – slowing from 85 days (FY13) to 108 days in FY15.

- Creditor days – the time taken to pay creditors – slowing from 77 days (FY13) to 84 days in FY15

- The cash conversion cycle slowing from 13 days to 38 days over the period.

The figure that really stands out is stock says. Dick Smith sold technology-based products that quickly become obsolete. I expected to see stock turning over at a much quicker pace. It is clear that the slow stock turnover also affected creditor payment timeframes. The comparison to JB Hi-Fi’s working capital cycle is telling.

The table below uses the FY13 cash conversion cycle to restate FY15’s working capital and then compares the restated and actual figures. The outcome is that the slowing cash conversion cycle resulted in Dick Smith using $80m more cash to support its growth, than should otherwise have been the case.

Leaving the business vulnerable to shocks

The summary of the Dick Smith story, in my opinion, is that its growth, combined with poor working capital management (particularly stock and creditors) meant it needed more funds than it should have, which reduced its margin for error and left it vulnerable to shocks.

As an aside, managing your relationship with your funders is particularly important in this circumstance. I think it is clear that Dick Smith did not do this well.

The lessons for owners of small and medium businesses

- Pay attention to your balance sheet, as well as your profit and loss statement;

- Learn how to construct and read a funds flow statement. It will tell you where your money is coming from and going to. It will help you understand why you sometimes feel like you are going broke whilst making a profit;

- Pay attention to your working capital. Regularly measure the length of time it takes to sell stock, collect debtors and pay creditors;

- Your working capital is often the largest investment in your balance sheet. Managing it well usually has a bigger impact on your cash flow than the earnings of your business;

- Benchmarking your business against competitors can provide thought provoking insights; and

- Managing your relationship with your funders is essential, particularly when times are tough.

Michael Stapleton is a founding member of the Association of Virtual CFOs. He operates a Melbourne-based Virtual CFO practice, helping owners of small and mid-size businesses understand the drivers of their cashflow and make financially informed decisions. Find out more about the Association of Virtual CFOs on LinkedIn.

Comments