Blackmores is Australia’s largest vitamin and supplement company in Australia. Its sales have more than doubled between the 2013 and 2016 financial years, which is rapid growth in anyone’s book. Profitability has followed growth, rising more than 300% over the same period

Growth is always tricky to manage and is often the thing that gets a business in trouble.

Read more: Murray Goulburn and the perils of serving two masters

So, I thought I would take a look at how well Blackmores has managed its growth to date and see if there are lesson to help owners of growing small and medium size businesses.

Using excess capacity

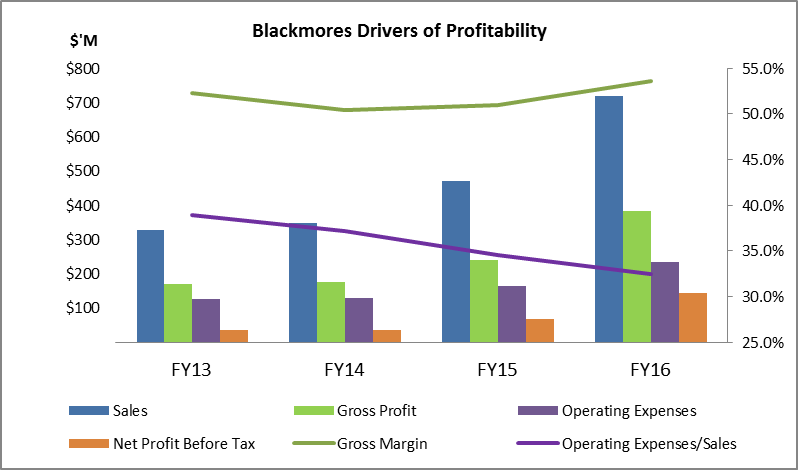

The chart below shows the trends in Blackmores’s sales, gross profit, gross margin, operating expenses and operating expenses as a percentage of Sales.

It’s a chart I use regularly because it helps business owners understand the factors that are driving their profitability. There are a number of points to note from this chart:

- The growth in sales, particularly between FY15 and FY16.

- An increasing gross profit (reflecting the increasing sales) but at a marginally lower gross margin in FY14 and FY15 (compared to FY13). Volume is driving the improved gross profit.

- Operating expenses increasing (reflecting the increasing sales) but at a slower rate than the growth in sales as indicated by the decline in operating expenses/sales.

- For a growing business, the gap between gross margin and operating expenses as a percentage of sales is a proxy for the profitability of the business. In FY13 and FY14 this gap was a little over 13%, before rising to 16.5% for FY15 and 21% for FY16.

This graph indicates that Blackmores has managed its growth well by using excess operational capacity to help support its growth. It’s a pretty good outcome.

Return on invested capital

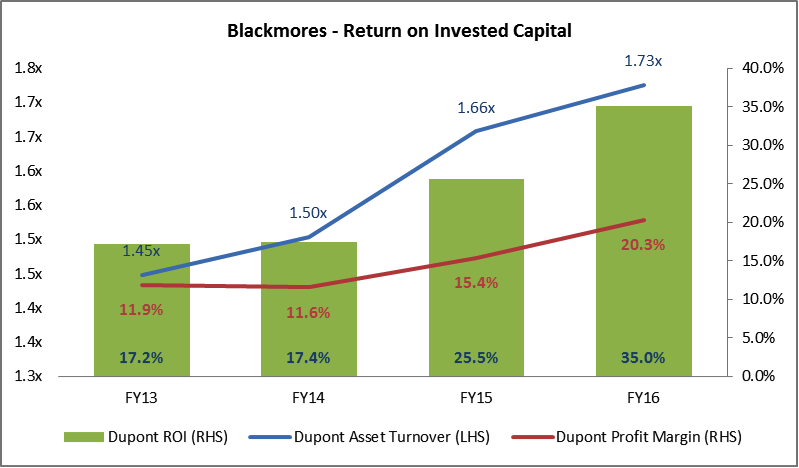

The next technique uses something called DuPont analysis. The objective is to determine more holistically how well Blackmores has been managing its growth.

DuPont analysis was invented during the 1920s by a salesman who worked for the DuPont Corporation. It’s useful in helping a business owner understand the factors driving the return on the capital they have invested in their business. It is particularly useful for companies that are highly capital-intensive; airlines, large retailers, manufacturers, transport companies and farms are examples of capital intensive businesses.

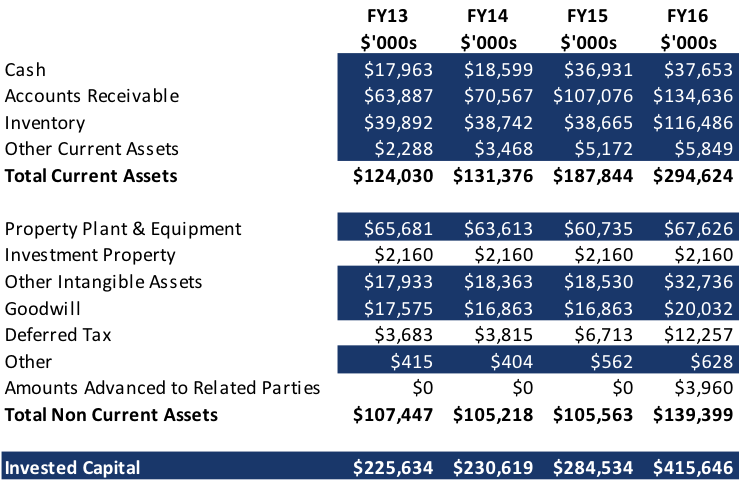

Invested capital is the aggregate value of all the assets used by a business to generate Sales. The table below summarises the assets of Blackmores. The assets highlighted in blue are those that are used to generate revenue.

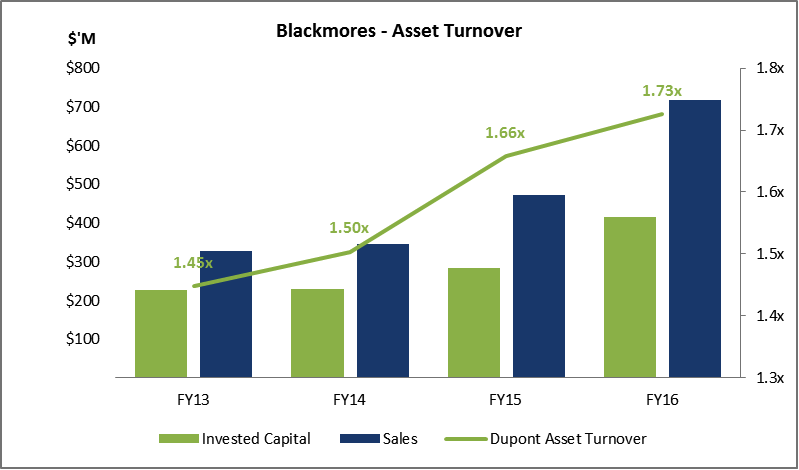

In the graph below invested capital is represented by the green columns, while revenue is represented by the blue columns.

You can see that both invested capital and revenue have been rising, but revenue has been increasing at a faster rate. This translates to a rising asset turnover ratio (green line), which occurs when the assets are being used more efficiently in terms of generating sales.

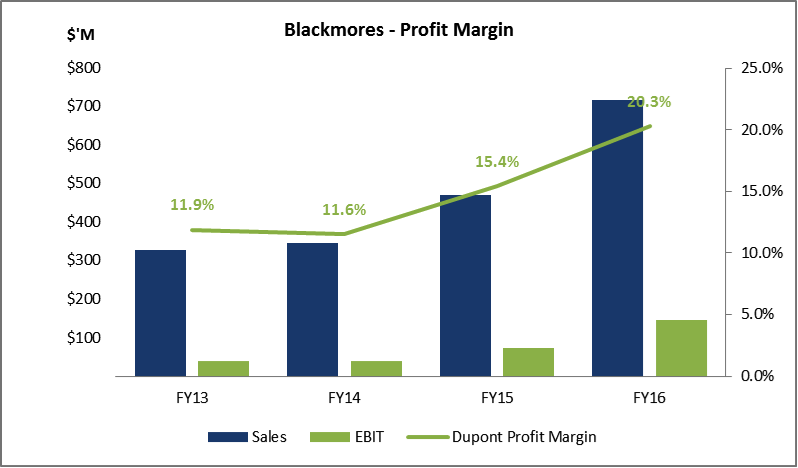

The next aspect of the DuPont process is to look at the profitability of the business. The graph below measures Blackmores’s earnings before interest and tax against its revenue. It is the outcome from the Drivers of Profitability Chart.

If we combine the asset turnover with the profit margin of Blackmores, we will get the return on invested capital. See below.

Both asset turnover and profit margin show improving trends and both contribute to an improving return on invested capital. Asset turnover was a more influential factor for the improved return on invested capital in FY14 and FY15, but in FY16 the profit margin is the more influential factor.

On this basis, you would conclude that growth has been managed well, both in terms of using excess capacity of plant and excess capacity of people.

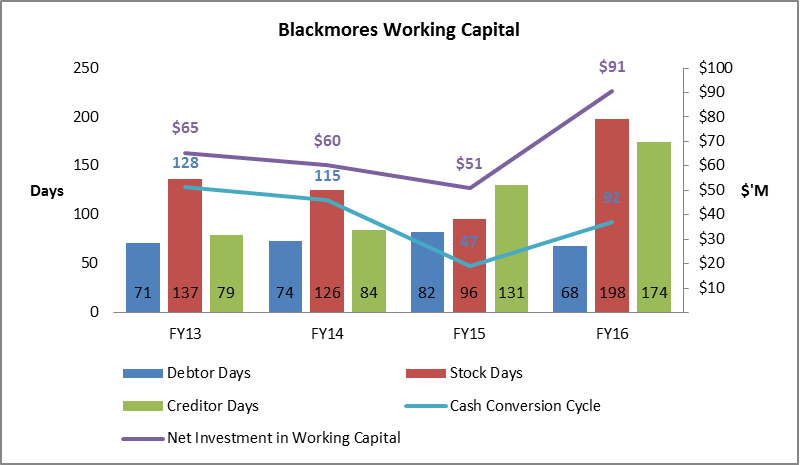

Working capital management

Let’s now take a look at working capital management.

The following graph is quite busy, so let’s work through it methodically.

The blue columns represent debtor days—the average number of days it takes Blackmores to collect their debtors.

The red columns represent stock days—the average number of days it takes Blackmores to sell its stock.

The green columns represent creditor days—the average number of days it takes Blackmores to pay its creditors.

The blue line is the cash conversion cycle—the average number of days it takes cash to cycle through the business. It is calculated as debtor days plus stock days, minus creditor days.

The purple line is the value of net working capital. It is calculated as the value of debtors plus the value of stock, less the value of creditors.

Between FY13 and FY15 the cash conversion cycle quickened from 128 days to 47 days. Over the same period, the net investment in working capital reduced from $65 million to $51 million. These are trends I would normally be happy to see, particularly for a growing business.

However, the improvement has been made partially from quickening the pace of stock turnover, but mainly by stretching creditors. As at FY15, Blackmores was taking more than four months to pay creditors. This is not sustainable for either party. An improving cash conversion and the net investment in working capital driven by stretched creditors is a low quality improvement.

In FY16, the cash conversion cycle and net investment in working capital spikes to 92 days and $91 million, respectively. A lengthening of inventory days (from 96 to 198 days) is the cause. Although creditors are stretched again to 174 days (almost 6 months) and debtors collected at a faster rate (from 82 days to 68 days) it is not enough to offset the significant increase in stock days.

There are some trends here, particularly in slowing stock turnover and slowing creditor payment time frames that are disturbing:

- If revenue growth continues then I would expect that the inventory days will begin to reduce back to more normal levels. However, if revenue was to stabilise or even fall, clearing through the very high level of inventory will be difficult and will likely require discounting, necessitating a hit to gross margin.

- The trend of extending creditors needs to reverse. These parties need to be paid and if you push them too far you can create a cash trap that unexpectedly bites you later on.

So, in terms of working capital management it looks to me like Blackmores has work to do.

The lessons for owners of growing small and medium size businesses

- Use both the profit and loss statement and balance sheet to help you understand how well you are managing growth;

- Understand whether the profit or loss of your business is being driven by gross margin, operating expenses/sales, or both;

- Keep an eye on your asset turnover ratio to determine if growth is being assisted by using excess capacity, particularly in your fixed assets;

- Understand the value of your invested capital and whether the return on that capital is being shaped by asset efficiency, operating efficiency or both. This will help you decide what actions need to be taken to help make growth sustainable; and

- Keep an eye on your working capital. It is often the biggest source and use of cash in a business. Managing working capital, particularly debtor collection and stock control, will help you fund your growth.

Michael Stapleton is a founding member of the Association of Virtual CFOs. He operates a Melbourne-based Virtual CFO practice, helping owners of small and mid-size businesses understand the drivers of their cashflow and make financially informed decisions. Find out more about the Association of Virtual CFOs on LinkedIn.

Comments