Economists were debating just two weeks ago whether COVID-19 could trigger an economic recession.

Now, they have accepted it as a reality.

The government has launched a series of ‘stimulus packages’ as a response to an increasingly ‘shut down’ economy and plummeting consumer confidence.

From a business perspective, so far we’ve seen:

- A $100,000 ‘cashback’ of PAYG Withholding, paid over a six-month period; and

- The guaranteeing of small business loans and loosening of credit to help SMEs fund losses.

$100,000 ‘cashback’ of PAYG withholding, paid over a six-month period

As a chartered accountant, business owner and advisor, my team and I have been at our battle stations for the last three weeks helping our clients navigate their financial challenges and all the available concessions from the federal and state governments.

All things considered, by far the most significant concession is the $100,000 PAYG cashback for SMEs.

I applaud the Morrison government for designing this delivery mechanism to give cash to SMEs, which is both efficient and scalable from the government’s perspective.

But it seems they spent too much time thinking about the delivery, rather than the concession itself.

It’s not enough.

Firstly, it’s only a cashback of the PAYG component for staff. Not gross wages, but the PAYG paid. My best guess is that the average marginal tax rate of employees of small businesses would be somewhere around 20% to 35% — which in effect means the government is subsidising the wage cost by this amount, capped at $100,000.

Oh yeah, and it’s paid over the next six months. Do you really expect any small business to survive that long with no revenue and the expectation to continue making payroll?

Compare this to the UK or Denmark which are subsidising the gross wages by 70% to 80% and you can see the massive difference.

Of course, something is better than nothing.

But the problem is, it isn’t even something if you already have a tax debt with the ATO.

It is not uncommon for the average small business owner to have some form of tax debt and payment plan with the tax office.

The core problem with this ‘cashback’ concession is that it won’t mean cash in the bank for a lot of small businesses. It simply offsets the existing debt with the ATO. And let’s not forget the GST that is still payable upon lodgement of these BAS anyway.

I would hazard a guess that the majority of small businesses wouldn’t see any of that $100,000 cashback in their actual bank account, but instead, less of a debt owing to the ATO.

Which brings us to the next stimulus measure.

Survive now, pay later

The second most significant ‘stimulus measure’ is the government guaranteeing 50% of new loans written by banks and SME lenders. This is coupled with providing an exemption from responsible lending obligations for lenders providing credit to existing small business customers.

Remember that royal banking commission we had like 18 months ago?

Yeah, Nah don’t worry about that.

Banks have also come to the party to provide repayment ‘holidays’ to ease short-term cash flow burden to keep businesses afloat and consumers keeping their home.

In this new world of economic uncertainty, borrowers can defer their loan repayments for up to six months.

Okay, yeah, this sounds generous in theory, but these debts need to be repaid eventually, and the interest still accrues!

Has anyone actually crunched the numbers on how deferring repayments impacts your loan?

I have…

The real cost of deferring repayments for six months

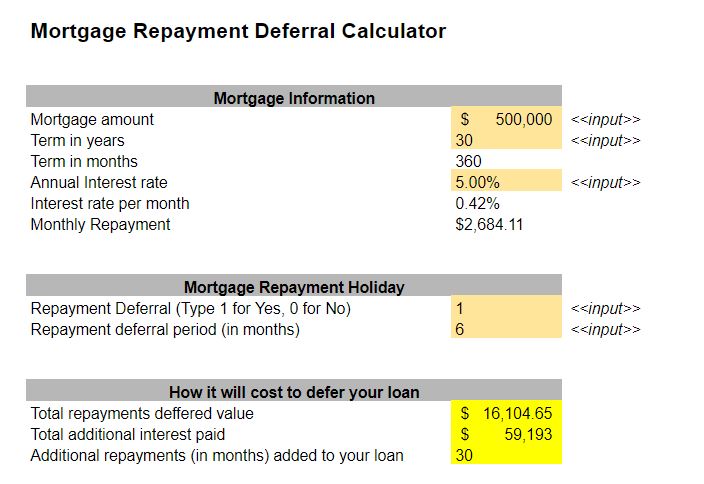

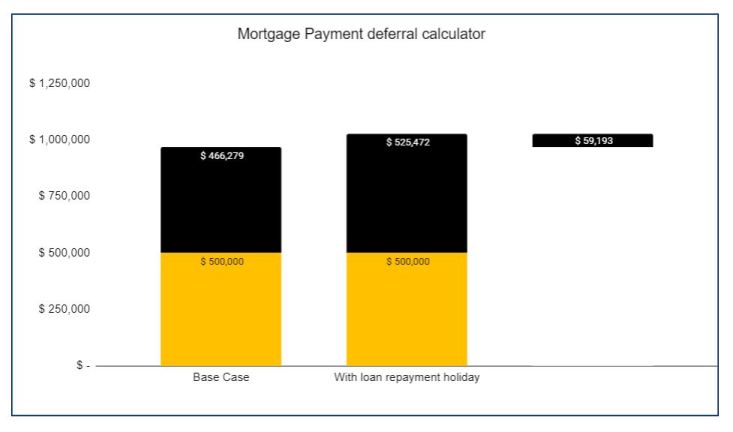

Let’s say you have a commercial business loan to the value of $500,000, payable over 30 years at a 5% interest rate and monthly repayments of $2,684.

Making no repayments for six months will put an additional $16,100 in your pocket to pay the rent and perhaps the payroll of staff you haven’t already made redundant.

The problem here is that the interest is simply being added to the loan balance, compounded monthly, which means you’re paying interest on interest. After this six-month holiday, the debt hangover really kicks in. You’ve accrued $59,000 of additional interest and added another 2.5 years to your loan term.

The exact same principle applies to your personal mortgage

If you’re considering getting a holiday on your home loan, use this calculator and crunch the numbers first.

Let’s be frank. The stimulus package by the government is not a stimulus package at all.

It’s a privatised debt trap.

Everyone is hoping the economy will miraculously bounce back in six months time when we emerge from social lock-down.

My fear is that perhaps a health crisis will be over, but a real financial crisis will have just begun.

Scott Morrison signalled more help is on the way. I truly hope it will be more effective than what we’ve seen thus far.

This article was first published on LinkedIn and has been republished with permission.

NOW READ: Businesses to “hibernate” through coronavirus crisis, Scott Morrison says

NOW READ: How self-employed people can prepare to weather the coronavirus storm

Comments