Insurance is one of the most challenging products in market. For marketers it is highly regulated, competitive and price driven, and for consumers, it is undifferentiated, complex and begrudged. That makes it perfect to scrutinise for some lessons in behavioural influence.

Design elements to overcome behavioural barriers

Most categories of insurance – including life, car, health and travel – suffer from all three of my core behavioural barriers:

- Apathy: people don’t want to think about it

- Paralysis: people get overwhelmed by options

- Anxiety: people don’t trust that the insurer will cover what they think is covered

To ensure they convince people to purchase, the insurers therefore rely heavily on how they communicate their offer. Design plays a key role in this.

It’s not easy to get right, though, so here are a couple of examples for travel insurance with ideas about what they’ve done well and need to improve.

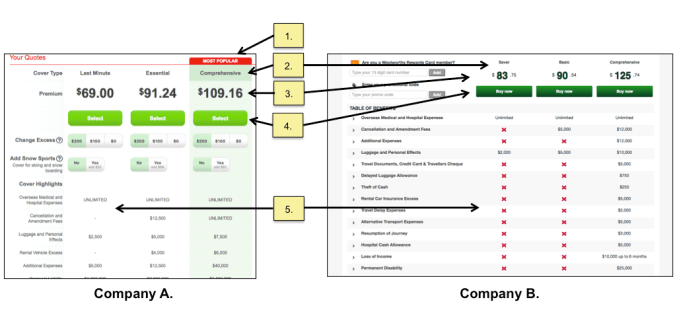

1. Most popular

Company A on the left includes a “most popular” tag on its comprehensive options to influence customer choices and reduce paralysis. “Most popular” and, to a lesser extent “Best Seller”, work because they signal what the social norm is in a particular context. When in doubt we tend to follow what others have done, so knowing which product is the most popular can help to pull a customer toward it.

2. Product names

Think very carefully about what name you give to your products because they influence both paralysis and apathy. Company A has called its products “Last minute”, “Essential” and “Comprehensive” and Company B has gone with “Saver”, “Basic” and “Comprehensive”.

As the top level of cover, “Comprehensive” is a suitable name. The interest is in the relativity between it and the other options.

If we assume the Company B wants to up-sell people to the Comprehensive option, the problem in calling the middle option “Essential” is that it may be interpreted in two ways: “must have” i.e. the most important bits, or “bare bones” i.e. just the essentials. If people believe the former rather than latter, the business has weakened its chances of up-selling.

In contrast, by calling their middle option “Basic”, Company A has left a question in the mind of their customer who now knows they are only getting the bare bones. This tension can help Company A up-sell to Comprehensive.

For the cheapest option Company B has chosen “Saver”, and Company A, “Last minute”. Neither is great. “Saver” risks customers feeling like they are not saving by going for the other options (risking down-grade), and “Last Minute” risks them feeling like they are paying more because it is urgent.

When it comes to your naming convention, your product names need to not only communicate what the product does when viewed in isolation, but what it does relative to others when appraised in a choice set.

3. Price sequencing and display

While it is important to be transparent about pricing, you do have choices about how you represent the actual numbers.

Both companies have chosen to sequence their prices from lowest to highest. The behavioural principle of anchoring suggests this is a mistake, and they would be better to lead with the most expensive option first. Why? When you read lowest to highest, the news only gets worse for the customer. When you read highest to lowest, the news gets better.

Another consideration is the typeface and size of your price. Company B has reduced the size of both the dollar sign and decimals – a behaviourally smart thing to do because it helps to diminish the perception of cost.

4. Calls-to-Action (CTA)

Company A asks people to “select” the product whereas Company B tells them to “buy now”. As insurance is a product that requires the customer to read product disclosure statements and provide personal information before finalising their contract, it is more appropriate to use a softer “select” CTA, signalling there is more to be done before you have to pay. “Buy now” escalates commitment, and as a result, anxiety, and therefore is only an appropriate CTA once the customer knows what they need to know and is ready to commit to the purchase.

5. Something to lose

Part of the art of up-selling customers is to create tension about the cheaper options. Company B does this through the overt use of red cross marks, a clever visual cue to let the customer know at a glance that they forfeit a lot of the Comprehensive benefits if they choose Saver or Basic. Company A misses out on building this tension by leaving the field blank.

For more ideas on how the three barriers to influence are impacting your business and how to design a solution, check out my book Behavioural Economics for Business.

Bri Williams runs People Patterns, a consultancy specialising in the application of behavioural economics to everyday business issues.

Comments